If you’ve ever looked at a medical bill or health insurance plan and thought, “Why am I still paying so much even though I have insurance?” you’re not alone. Many people first encounter the term coinsurance when they receive an unexpected bill after a doctor visit or hospital stay. At that moment, the word feels confusing, technical, and frustrating. That’s exactly why so many people search what does coinsurance mean.

The good news is that coinsurance is not as complicated as it sounds. Once you understand how it works, you can better predict healthcare costs, compare insurance plans, and avoid surprises.

Quick answer:

Coinsurance is the percentage of medical costs you pay after meeting your deductible, while your insurance company pays the rest.

What Does Coinsurance Mean in Health Insurance?

To understand the coinsurance meaning, think of it as cost-sharing between you and your insurance provider.

In most health insurance plans, you don’t just pay premiums. You also share costs when you receive care. Coinsurance defines how that cost is split.

Simple definition:

Coinsurance is the percentage of a covered medical bill that you pay after your deductible is met.

For example:

- Your plan has 20% coinsurance

- Insurance covers 80%

- You pay the remaining 20%

In short:

Coinsurance = percentage-based cost sharing after deductible

This is why many people also search for what is coinsurance in health insurance—it directly affects how much money comes out of your pocket.

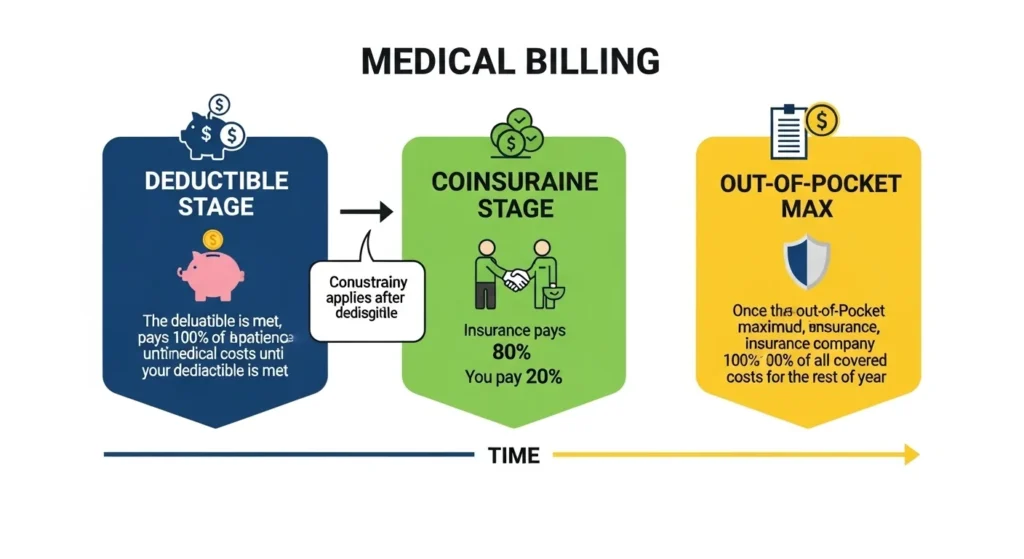

How Does Coinsurance Work? (Step by Step)

Understanding how does coinsurance work is key to avoiding confusion.

Here’s the typical order of costs in a health insurance plan:

- Premium – What you pay monthly to keep coverage

- Deductible – What you pay before insurance starts paying

- Coinsurance – Percentage you pay after deductible

- Out-of-pocket maximum – The most you’ll pay in a year

Step by step example:

- Deductible: $1,000

- Coinsurance: 20%

- Medical bill: $2,000

What happens?

- You pay the first $1,000 (deductible)

- Remaining bill: $1,000

- Your 20% coinsurance = $200

- Insurance pays $800

This type of coinsurance example shows why medical bills can still feel expensive even after insurance helps.

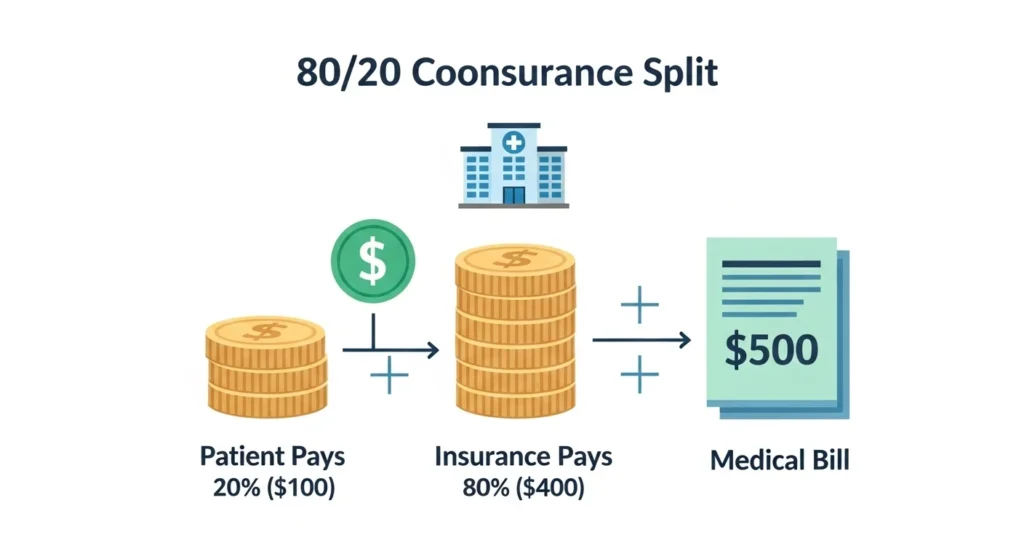

What Does 80/20 Coinsurance Mean?

One of the most common questions people ask is: what does 80/20 coinsurance mean?

An 80/20 coinsurance split means:

- Insurance pays 80%

- You pay 20%

So if a covered service costs $500:

- Insurance pays $400

- You pay $100

The coinsurance percentage can vary by plan and service, so it’s important to check your policy details.

Coinsurance After Deductible: Why Timing Matters

A key detail many people miss is that coinsurance applies after the deductible.

That means:

- Before your deductible → you usually pay 100%

- After deductible → coinsurance starts

- After out-of-pocket max → insurance pays 100%

This is why you’ll often see the phrase coinsurance after deductible in policy documents and medical billing statements.

Coinsurance in Medical Billing

You’ll most often see coinsurance in medical billing on documents like:

- Explanation of Benefits (EOB)

- Hospital invoices

- Insurance claim summaries

A typical line might say:

“Patient responsibility: 20% coinsurance”

This tells you exactly which portion of the bill you owe. Understanding this language helps you verify bills and avoid overpaying.

Coinsurance vs Copay: What’s the Difference?

Many people confuse coinsurance vs copay, but they work differently.

| Feature | Coinsurance | Copay |

| Type | Percentage | Fixed dollar amount |

| Example | 20% of bill | $30 per visit |

| Cost varies? | Yes | No |

| When used | After deductible | At time of visit |

A copay stays the same, but coinsurance changes depending on the total cost of care.

Coinsurance vs Deductible: Not the Same Thing

Another common comparison is coinsurance vs deductible.

| Term | What It Means |

| Deductible | Amount you pay before insurance starts |

| Coinsurance | Percentage you pay after deductible |

Both affect your total healthcare spending, but they apply at different stages of coverage.

Why Do Insurance Plans Use Coinsurance?

Insurance companies use coinsurance to:

- Share costs between insurer and patient

- Keep monthly premiums lower

- Encourage mindful healthcare use

While coinsurance can increase out-of-pocket costs, plans with higher coinsurance often have lower premiums. It’s a trade-off.

This is why health insurance coinsurance explained is such an important topic for consumers choosing a plan.

How to Reduce Coinsurance Costs

While you can’t eliminate coinsurance completely, you can manage it better:

- Choose in-network providers

- Compare plans with lower coinsurance percentages

- Understand your out-of-pocket maximum

- Ask for cost estimates before procedures

- Use preventive services (often 100% covered)

Being informed gives you more control over medical expenses.

Similar Health Insurance Terms You Should Know

Understanding coinsurance is easier when you know related terms:

| Term | Meaning | When It Applies |

| Premium | Monthly insurance payment | Always |

| Deductible | Pay before insurance helps | Early |

| Coinsurance | Percentage you pay | After deductible |

| Copay | Fixed visit fee | Per service |

| Out-of-pocket max | Spending limit | Yearly |

FAQs About Coinsurance

Q. What does coinsurance mean in simple words?

It means you and your insurance company split medical costs by percentage after your deductible.

Q. Is coinsurance paid every time?

Yes, for covered services, until you reach your out-of-pocket maximum.

Q. Can coinsurance be 0%?

Yes. Some plans offer 0% coinsurance, meaning insurance pays 100% after deductible.

Q. Is coinsurance the same for all services?

No. Different services (hospital, prescriptions, specialists) may have different coinsurance rates.

Q. Why is my bill high even after insurance?

High coinsurance percentages and large medical bills can still result in significant out-of-pocket costs.

Conclusion

Understanding what does coinsurance mean is essential for managing healthcare expenses wisely. Coinsurance is not a hidden fee it’s a defined percentage that explains how costs are shared after your deductible is met.

By learning the coinsurance definition, seeing real world examples, and knowing how it compares to copays and deductibles, you can make smarter insurance decisions and avoid costly surprises.

The more you understand coinsurance, the more confident you’ll feel navigating medical bills and insurance plans.